MEAT+POUTRY, in partnership with the North American Meat Institute, commissioned Kansas City, Mo.-based Cypress Research to conduct the 2023-24 Meat and Poultry Industries Capital Spending Trends Study.

Among some of the goals of the project were to collect information from meat and poultry processors about the outlook of their companies and the industry as a whole.

Besides gathering information about plans for general capital spending, the survey looked specifically at the categories of the planned investments and the goals and motivations behind them.

The survey also identified key business challenges in the industry and market that influenced investment decisions.

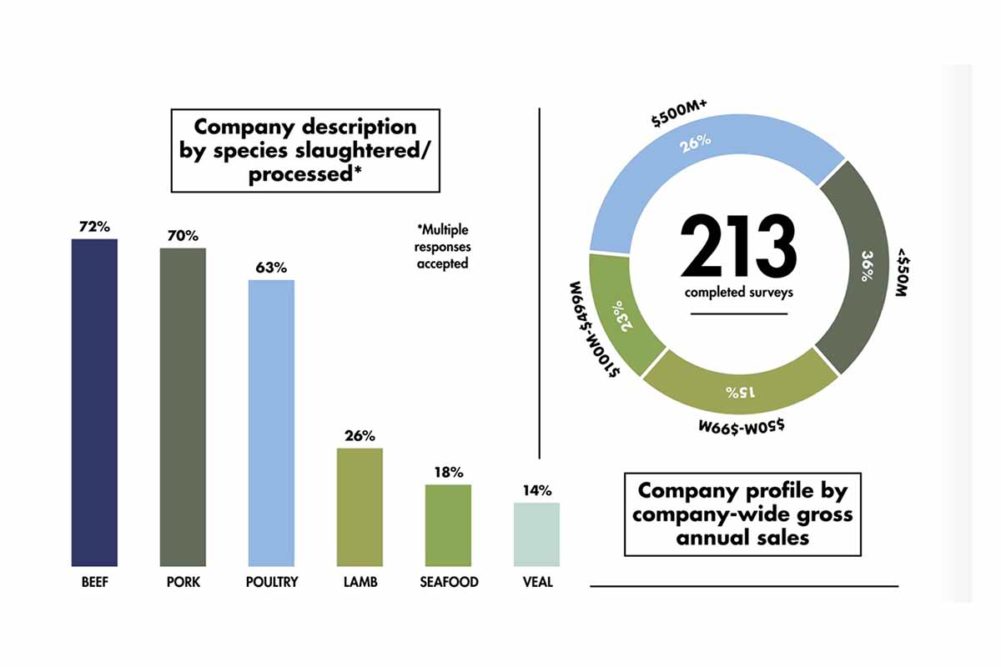

Surveys were completed by industry professionals whose role at their companies included capital spending decision making. The data reflects the findings of surveys of 213 of people in those roles.

Source: Sosland Publishing Co.

Source: Sosland Publishing Co.The results suggest that most processors are facing many of the same challenges, which have resulted in some of the industry’s highest profile meat and poultry companies reporting financial losses in the hundreds of millions of dollars in 2023.

“Processors are facing the ongoing labor crunch, high raw material costs, and less consumer demand for meat,” said Marjorie Hellmer, president of Cypress Research. “These and an array of other issues are contributing to the financial challenges on full display in the US meat and poultry industry.”

In terms of operation types of the companies represented, 94% of them were from processing companies and about 44% said their operations included slaughtering.

As for company size represented by the respondents, 51% were companies with annual sales under $100 million, while 49% were from companies with sales of more than $100 million (which included 26% from companies with sales of more than $500 million), with the vast majority of them processing beef, pork and poultry products.

Job roles of the majority of respondents were senior executive-level managers (31%) or operations executives (26%).

Most respondents (88%) said their company’s outlook for 2024 was positive, and 76% said their outlook for the industry is positive for the coming year.

Over 40% reported a trend toward more capital spending in the current year over 2022 levels. In terms of amounts, respondents said average 2023 capital spending represented just under 11% of their companies’ annual revenues.

When asked about how their companies’ capital investments compared to previous years, 41% of the companies represented in the survey reported increases in 2023 compared to 2022 levels. This was especially true of those companies with annual sales of over $100 million (46%).

When asked about the ratio of capital expenditures to company sales, respondents said the average is 10.9% of revenues this year and project that to increase to 11.4% in 2024.

Of that capital spending budget 26% was earmarked for investments in equipment. Seven out of 10 respondents said 2024 plans include investments in new processing equipment and maintenance/replacement parts.

Packaging equipment and cold storage technology were part of the plans for investments of 60% of companies.

The top 4 reasons and goals for capital spending included:

- Quality and consistency improvement

- Enhancing processing capabilities

- Increasing production capacity

- Improving food safety

In an era when input costs and maintaining adequate staffing are common headwinds among most processing companies, it shouldn’t come as a surprise that among the top business concerns of industry professionals are “Attracting and retaining a quality workforce” (69% of respondents), “Labor costs” (69%) and “Increased raw material costs” (61%). Somewhat surprisingly, “Food safety” ranked sixth at 40% and “Cybersecurity” ranked even lower, at 24%.

Hellmer said it isn’t uncommon in the food sector for stakeholders to focus their attention and dollars to address the most obvious headwinds, but food safety is always a concern.

“Generally, trends in survey research with food manufacturing professionals show that the concerns for food safety don’t beat those perennial challenges tied directly to business operations such as attracting and retaining talent and the cost of inputs,” she said. “The United States also continues to struggle to control inflation. Combine this with global instability and other macro-economic pressures, and these challenges are top-of-mind for meat and poultry processors.”

When turning specifically to the topic of company capital investing, building stronger and more efficient food safety elements into their operations is definitely a key goal in processor planning. According to this study, when asked for their companies’ 2024 capital investing goals, objectives were led by improving product quality and process capabilities, increasing capacity for existing products and improving food safety.

Among the top areas processing companies said they planned to invest in during 2024, new processing equipment along with maintenance and replacement parts (both at 74% of respondents) topped the list followed by investing in systems improvements, including system integration and automation (69%). Meanwhile, one of the more automated parts of many processing plants, packaging, was identified as the area targeted for equipment investments among 61% of respondents.

“An important tool processors can use to help manage and mitigate some of these difficulties is a continued commitment to investing in equipment and technologies — even during tough times,” Hellmer said. “Automation can help ease the labor shortage and make operations more efficient while also providing greater protections for workers.”